[ad_1]

Quarter in Overview

As we wrap up 2022, it’s actually been one for the historical past books. Throughout the globe, inflation spiked to ranges not seen in many years. Europe was (and nonetheless is) wracked by the most important battle there since 1945. The COVID pandemic is lastly moderating however continues to impression hundreds of thousands, whilst China relaxed its draconian COVID restrictions. And U.S. capital markets had one of many worst years on file, with bond costs falling greater than any 12 months since 1974. It’s been an attention-grabbing 12 months, to say the least.

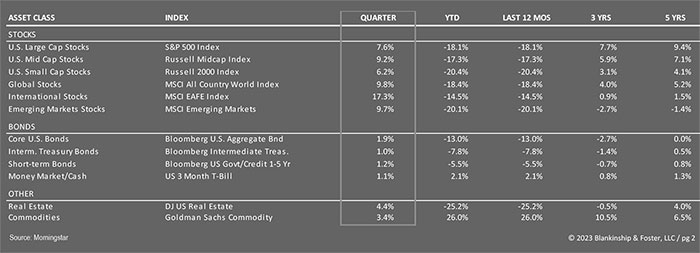

2022 was the worst 12 months for shares and bonds collectively since 2008 and the third worst since 1974. Few investments had been optimistic final 12 months apart from money. Regardless of gaining 7.6% within the fourth quarter, the S&P 500 Index of huge U.S. corporations fell 18.1% for the 12 months. Smaller corporations, represented by the Russell 2000 Index, rose 6.2% within the quarter, off 20.4% for the 12 months. The MSCI EAFE Index of shares of corporations in developed nations outdoors the U.S. gained 17.3% within the quarter because the greenback reversed course and fell. Worldwide shares had been nonetheless off 14.5% for the 12 months. The bond market had a little bit of a reprieve as nicely with the 10-year Treasury yield little modified in the course of the quarter. The Bloomberg U.S. Combination index gained 1.9% within the fourth, reducing its year-to-date loss to “solely” 13.0%. Excessive yield “junk” bonds had been off 11.2% for the 12 months and the Dow Jones US Actual Property Index completed the 12 months down 25.2%. Money and commodities had been the one shiny spots for the 12 months, up 2.1% and 26.0% respectively. Regardless of the blockbuster 12 months for commodities, the S&P GSCI commodity index is down 3.3% per 12 months for the final 10 years together with this current optimistic efficiency, so this 12 months’s acquire got here at a major long-term value.

Financial system

Trying forward, let’s begin with some excellent news. Inflation is lastly moderating, with the newest studying of the Client Worth Index at “solely” 7.1% year-over-year. The inflation spike final 12 months was brought on by a poisonous mixture. Throughout the COVID pandemic, lots of people had been caught of their houses shopping for items as an alternative of companies. Snarled provide chains meant these items couldn’t make it from factories to customers, so costs elevated. On the identical time, the U.S. coverage response poured cash into shopper and enterprise coffers, including gas to the fireplace. Lastly, Russia’s invasion of Ukraine induced an enormous spike within the value of meals and vitality. Core items value inflation has largely eased, as have meals and vitality costs. Analysts anticipate this development to proceed as provide chains are largely repaired however shopper spending is slowing down, decreasing demand for the resupplied items.

Labor demand stays strong, with the ratio of job openings to job seekers near 1.7, a traditionally excessive stage. Corporations which have had such a tough time hiring staff for the final two years could also be extra reluctant to allow them to go if the financial system does gradual this 12 months. In any occasion, with unemployment nonetheless operating close to a traditionally low stage, it’s laborious to say we’re in a recession in the meanwhile. Unemployment is a lagging indicator and does sometimes rise in a recession, however a mix of COVID deaths, early retirements and decreased immigration have created an enormous scarcity of staff. It’s laborious to think about a state of affairs the place unemployment will increase considerably.

Financial development seems strong within the fourth quarter, although slowing into 2023. The Federal Reserve Financial institution of Atlanta’s GDP Now estimator reveals a studying of roughly 4.1% development for the fourth quarter, however most analysts we learn anticipate a recession to start someday throughout 2023. That is supported by an inversion within the Treasury Yield curve. When longer-dated bonds yield greater than short-term bonds, it’s a dependable indicator {that a} recession is coming. But it surely isn’t a really well timed indicator, as it may be a number of quarters earlier than a recession truly begins.

With that stated, most appear to anticipate a comparatively gentle recession reasonably than a pointy drop in exercise. JP Morgan likened it extra to “strolling right into a swamp than falling off a cliff”. So we wouldn’t be shocked to listen to the “R” phrase much more in coming months, and traders will definitely be in search of clues as to the path of the financial system and by extension, company earnings.

Outlook

As we wrote final month, the present growth is slowing however nonetheless appears to have some momentum. We do anticipate the Federal Reserve to lift rates of interest at their subsequent assembly, and presumably the next one, however these will increase must be extra muted. Bond traders seem like anticipating charges to start falling by the top of the 12 months, seemingly on account of a recession forcing the Fed to decrease rates of interest once more.

As we identified final quarter, the everyday post-war recession has lasted about 10 months and resulted in a drop of about 3% of Gross Home Product. Housing, the epicenter of the final recession, and household steadiness sheets are in higher form this time round. Additionally, at the moment’s tight labor market may additionally serve to dampen the impression of a possible recession.

Our dashboard reveals a variety of warning lights, however no shiny pink warnings but. Company earnings estimates don’t appear to have absolutely absorbed the dangers of recession, so there’s seemingly draw back threat to inventory costs within the near-term, nevertheless it’s practically unattainable to foretell when that may occur or how far costs could fall.

Trying ahead, present valuations on shares and bonds are extra enticing than they’ve been in years. 5 12 months anticipated returns on investments have improved considerably, although we are able to’t rule out falling costs (and thus improved future returns) within the coming months. We’d not be shocked by a drop in inventory costs adopted by a powerful restoration by year-end, although different situations are additionally doable.

Our Portfolios

Our inventory publicity is at the moment broad primarily based and weighted in direction of massive U.S. corporations. Our price bias has helped enhance efficiency regardless of the broad weak point of U.S. inventory markets final 12 months. Our worldwide publicity benefitted from our mix of foreign money hedged investments, which outperformed because the greenback strengthened earlier within the 12 months, and unhedged positions which soared within the fourth quarter. Improved valuations (a lot lower cost to earnings multiples) counsel that shares are poised for higher efficiency over the subsequent 5 to 10 years, however a recession within the coming months or quarters will delay the beginning of any restoration in fairness costs.

Immediately’s increased rates of interest imply that anticipated bond returns going ahead are considerably higher than they had been this time final 12 months. Extra importantly, if our expectation of a recession is realized, rates of interest will seemingly settle again down, offering good returns to bonds, which ought to assist if shares falter heading right into a recession. This might be a welcome change from 2022 when bonds fell virtually as a lot as shares.

Briefly, we anticipate extra volatility in 2023 as traders put together for a doable recession and regulate their estimates for inventory costs accordingly. We’ll use such durations of volatility to rebalance portfolios and choose up shares (or bonds) at discounted costs, to raised revenue from the restoration that has adopted each main market decline.

As at all times, we’re right here for you and are prepared to offer the steerage and planning you anticipate from us. You probably have any questions on your investments or your monetary plan, we’d love the chance to debate them with you.

Going Inexperienced

We’ve got been working with our know-how distributors and are excited to announce that we’re in a position to ship your quarterly stories to you by way of our safe on-line portal. This can assist to save lots of paper and is definitely safer, since you may solely entry the stories by means of a safe web connection.

If you need to save lots of a number of timber (and make the stories obtainable everytime you’re able to learn them), then please electronic mail your advisor and ask about changing your stories to digital supply.

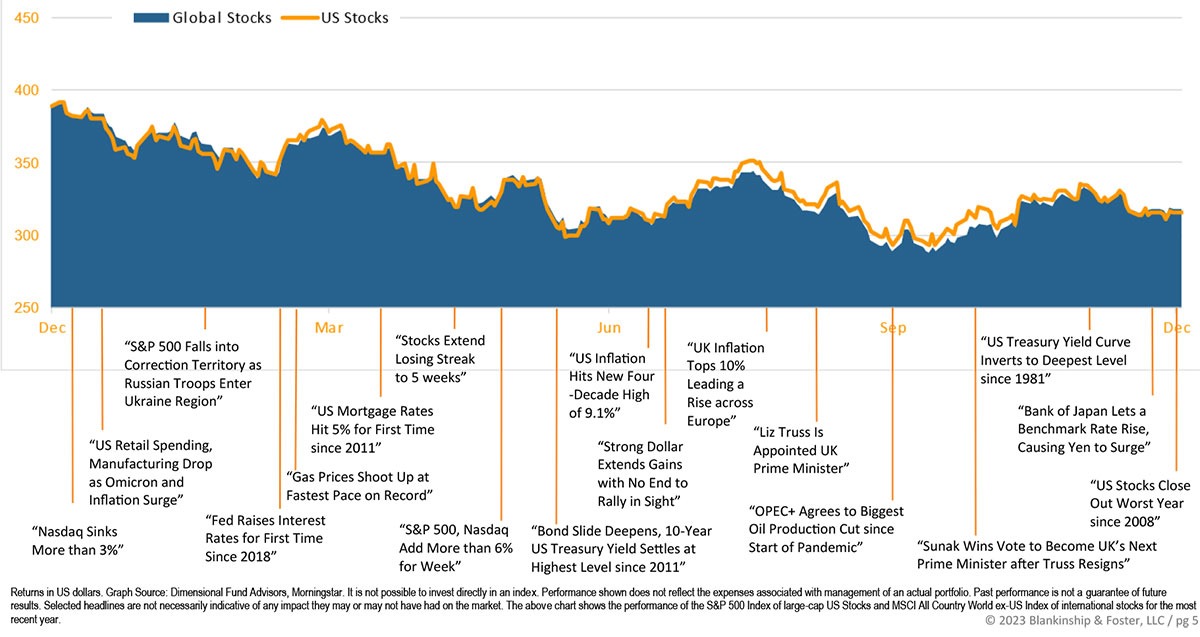

International Inventory Market Efficiency

The chart under reveals the change in international fairness markets all year long. Juxtaposed over the market efficiency are a few of the key occasions that occurred in the course of the interval. Generally as we get to the top of a unstable interval, it’s tough to look again and bear in mind every little thing that occurred alongside the way in which.

DISCLOSURE:

Previous efficiency is just not a sign of future returns. Data and opinions offered herein replicate the views of the writer as of the publication date of this text. Such views and opinions are topic to vary at any level and with out discover. Among the info offered herein was obtained from third-party sources believed to be dependable however such info is just not assured to be correct.

The content material is being offered for informational functions solely, and nothing inside is, or is meant to represent, funding, tax, or authorized recommendation or a suggestion to purchase or promote any sorts of securities or investments. The writer has not thought-about the funding goals, monetary state of affairs, or explicit wants of any particular person investor. Any forward-looking statements or forecasts are primarily based on assumptions solely, and precise outcomes are anticipated to fluctuate from any such statements or forecasts. No reliance must be positioned on any such statements or forecasts when making any funding resolution. Any assumptions and projections displayed are estimates, hypothetical in nature, and meant to serve solely as a suggestion. No funding resolution must be made primarily based solely on any info offered herein.

There’s a threat of loss from an funding in securities, together with the danger of complete lack of principal, which an investor will must be ready to bear. Various kinds of investments contain various levels of threat, and there might be no assurance that any particular funding will probably be worthwhile or appropriate for a selected investor’s monetary state of affairs or threat tolerance.

Blankinship & Foster is an funding adviser registered with the Securities & Alternate Fee (SEC). Nonetheless, such registration doesn’t indicate a sure stage of ability or coaching and no inference on the contrary must be made. Full details about our companies and charges is contained in our Type ADV Half 2A (Disclosure Brochure), a replica of which might be obtained at www.adviserinfo.sec.gov or by calling us at (858) 755-5166, or by visiting our web site at www.bfadvisors.com.

[ad_2]