[ad_1]

It takes a whole lot of planning to design a profitable retirement technique. Saving and investing sufficient to fund a cushty retirement is important, however there are different issues to think about as properly. Your life-style, the place you’ll reside, medical bills, pension, and Social Safety are all items of the retirement puzzle.

One facet of retirement planning that always will get missed is tax planning. Taxes can have an actual impact in your retirement, and never planning for them may cause large surprises. Listed below are some widespread tax surprises that retirees come throughout, and what you are able to do to keep away from them.

Retirement plan distributions

When you have diligently added to your financial savings and investments through the years, congratulations! Probably the greatest methods to maximise financial savings is to designate a portion of your pay to robotically go into 401(okay)s, IRAs, or different retirement plans. If that deferred pay goes to a “pre-tax” (not a Roth) plan, then taxes on the pay might be deferred. This lowers your tax invoice within the working years and helps create room in your funds for greater financial savings.

Nevertheless, this will also be one of many largest tax surprises for retirees, because the tax is due while you withdraw cash from the accounts. If these “pre-tax” retirement accounts are your foremost supply of earnings early in retirement, you might end up in a excessive tax bracket. This could get actually painful in case your solely option to pay the taxes on the distributions is by taking much more distributions from them. Clearly, realizing what you’ll pay taxes on in retirement is a key a part of a profitable retirement plan.

Capital beneficial properties

Investments held in non-retirement plan accounts take pleasure in useful tax remedy within the type of decrease tax charges. Certified dividends and long-term (a couple of yr) capital beneficial properties are taxed at a 15-20% tax price — and even 0%, relying in your earnings. Build up financial savings in non-retirement accounts can present an actual profit in retirement. You possibly can withdraw cash from these accounts with much less tax price. Nevertheless, the capital beneficial properties that construct up in long-term investments are taxable when they’re realized (offered). These can actually add up if sufficient are offered throughout the yr. Mixed with different sources of earnings, you’ll be able to find yourself with greater tax charges on these beneficial properties, lowering the tax benefit.

Social Safety

Social safety advantages in retirement could also be partially taxable, principally taxable, or not taxable in any respect. It is dependent upon your “mixed earnings” for the yr. For a pair submitting taxes collectively, none of your and your partner’s advantages are taxable in case your mixed earnings is lower than $32,000. 50% of the advantages are taxable if earnings is between $32,000 and $44,000, and 85% of the advantages are taxable if earnings is greater than $44,000. As you’ll be able to see, a rise of just some thousand {dollars} in earnings may cause an surprising enhance in your taxes in retirement.

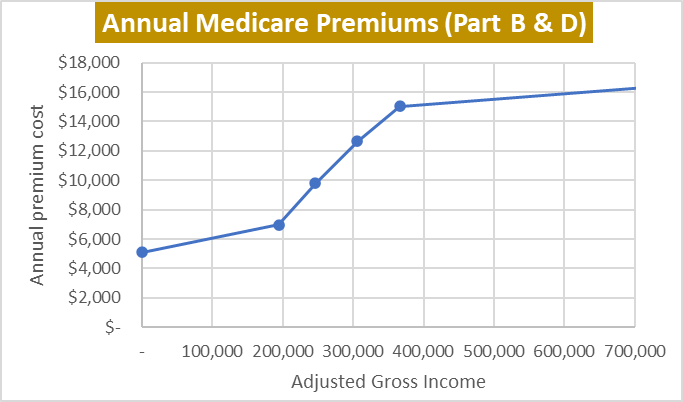

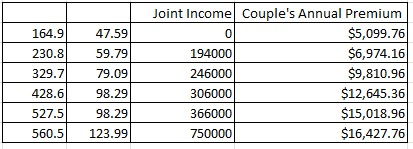

Medicare premium surcharges

Medicare is the first medical insurance for hundreds of thousands of retirees aged 65 and over. Unique Medicare (components A and B) covers most hospital and medical prices. Different components of Medicare (Half C, Half D, and Medigap) are personal insurance policy can present extra protection. Half A has no premium, however all the opposite components contain a premium.

The essential Half B premium is $164.90 monthly for 2023. Nevertheless, added premium surcharges known as income-related month-to-month adjustment quantities (IRMAA) can greater than double your Half B and half D premiums. IRMAA surcharges are based mostly in your whole earnings, so whereas they don’t seem to be technically a tax, they act like a tax. As an example, a pair submitting a joint tax return with earnings beneath $194,000 will sometimes have Half B and Half D premiums of about $5,000 for the yr. Nevertheless, if their earnings is over $194,000, IRMAA surcharges can elevate their whole premiums to over $16,000 a yr.

How you can cut back the shock issue

Having much less tax surprises in retirement means planning your retirement upfront. This implies planning for which accounts to attract from, and which pension, social safety, and Medicare choices to decide on. It additionally means being cautious about tax-generating actions like retirement plan distributions and capital beneficial properties. This typically requires a deeper have a look at all of the areas of your funds to make interconnected monetary choices.

At Blankinship & Foster, we concentrate on constructing an built-in plan centered on the monetary and life outcomes you really need. We take into account all of the vital items of the retirement puzzle, together with taxes.

Disclosure: The opinions expressed inside this weblog publish are as of the date of publication and are offered for informational functions solely. Content material won’t be up to date after publication and shouldn’t be thought of present after the publication date. All opinions are topic to alter with out discover, and as a consequence of modifications out there or financial circumstances might not essentially come to cross. Nothing contained herein must be construed as a complete assertion of the issues mentioned, thought of funding, monetary, authorized, or tax recommendation, or a suggestion to purchase or promote any securities, and no funding determination must be made based mostly solely on any info offered herein. Hyperlinks to 3rd celebration content material are included for comfort solely, we don’t endorse, sponsor, or suggest any of the third events or their web sites and don’t assure the adequacy of data contained inside their web sites.

[ad_2]