[ad_1]

Quarter in Evaluation

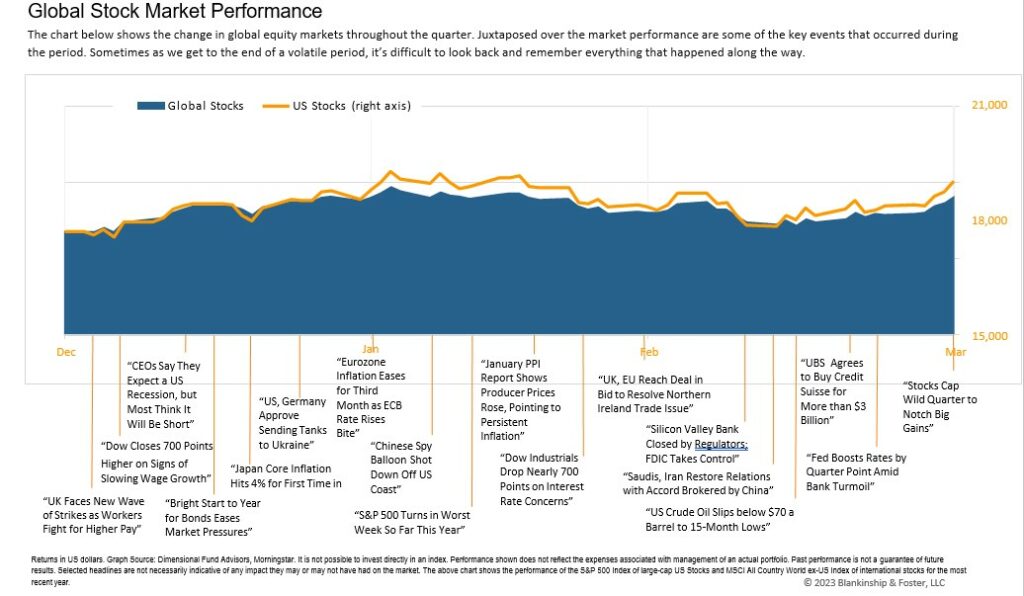

The massive story within the first quarter of 2023 was the failure of Silicon Valley Financial institution, Credit score Suisse and two different regional banks, representing the most important banks to fail since 2008. This brought on a quick interval of instability within the capital markets and in banking particularly, however it additionally possible had a longer-term affect on the supply of credit score to companies and shoppers alike. Extra on that in a bit. Whereas the economic system grew at about 2.6% within the fourth quarter of 2022, it possible slowed a bit within the first quarter of 2023, with the Federal Reserve Financial institution of Atlanta’s GDP Now estimate at about 1.5% on April 5.

Considerably counterintuitively, Buyers largely cheered the slowing economic system as a result of a slowing economic system makes it much less possible that the Federal Reserve will increase rates of interest additional. Regardless of the volatility surrounding the financial institution failures, capital market returns have been largely optimistic in the course of the quarter. The S&P 500 Index of enormous U.S. firms rose 7.5% within the first quarter. Smaller firms, represented by the Russell 2000 Index, gained simply 2.7% whereas worldwide shares represented by the MSCI EAFE Index rose 8.5%. The bond market benefitted from the sense that important additional rate of interest hikes have been unlikely. The benchmark 10-year Treasury yield fell barely to three.48%, leading to a acquire for many bond classes. The Bloomberg U.S. Mixture index gained 3.0% within the quarter whereas Excessive Yield “junk” bonds rose 3.7%. The Dow Jones US Actual Property Index rose 1.6% whereas final yr’s star asset class, commodities, dropped 4.9%.

Economic system

As soon as once more, the economic system is just not at present in a recession. Trying on the indicators that the Nationwide Bureau of Financial Analysis (which determines when recessions start and finish), it’s clear that the economic system remains to be rising, although at a slower tempo than within the fourth quarter. Many indicators are softening, equivalent to private incomes, industrial manufacturing and client spending, however to not the purpose of going into reverse.

Inflation continued to reasonable in the course of the quarter, falling from 7.8% year-over-year development in October to six.0% in February. Most forecasters count on a continued downward development in inflation over the course of the yr, presumably ending the yr round 4%.

The labor market stays sturdy however is dropping some momentum, although unemployment stays stable at round 3.5%. Wage development has eased and layoff bulletins are ticking up, signaling some future weak point in employment within the months forward. A cooling labor market ought to proceed to place downward strain on inflation, that means the Federal Reserve (Fed) could not need to proceed to lift rates of interest as quick as they’ve over the previous yr.

One other issue that can affect the Fed’s considering was the failure of some regional banks in the course of the quarter as a result of these failures have been brought on partially by the Fed’s rate of interest hikes. To be clear, as one financial institution government advised us, the elemental problem was that these banks “failed banking 101” by failing to handle their rate of interest threat and failing to diversify their depositor base. However it did expose some weaknesses within the banking system, forcing the Fed to ease up on the brakes a bit. From the Fed’s perspective, financial institution executives will possible be extra stringent in who they lend cash to going ahead, so a few of the work of slowing the economic system could also be carried out by bankers tightening lending requirements quite than by the Fed elevating rates of interest. The result is more likely to be the identical: considerably slower development within the months forward.

Greater rates of interest proceed to place strain on the housing market, whereas adjustments in Federal spending additionally affect the economic system. Whereas it’s typically a very good factor that the Federal price range deficit is reducing as a proportion of the economic system, it does imply that the federal government is spending much less cash and thus offering much less help for the economic system going ahead. It’s necessary to keep in mind that large federal authorities outlays in the course of the pandemic did contribute to inflation. However like a sugar excessive that’s worn off, decreased federal spending in the present day is a drag on present financial exercise.

Globally, central banks outdoors the U.S. have raised rates of interest whereas manufacturing exercise is softening within the U.S., Asia and Europe, at the same time as Companies stay sturdy. Apparently, charges are anticipated to fall quicker within the U.S. than overseas, presumably placing downward strain on the greenback and making worldwide investments extra engaging.

Outlook

Many elements have contributed to a slowing economic system, and it’s not a foregone conclusion {that a} recession should happen. However it does appear extra possible, and the consensus appears to level to a recession starting someday this yr, however once more this isn’t sure. As soon as once more, our dashboard exhibits a number of warning lights, however no vivid pink indicators. 12 months-over-year company income have fallen dramatically over the previous yr, and company spending on big-ticket investments are more likely to observe quickly.

Trying ahead, present valuations on shares and bonds are extra engaging than they’ve been in years. The five-year anticipated returns on investments have improved considerably, although we will’t rule out falling costs (and thus improved future returns) within the coming months if a recession does happen. Though shares have risen just lately, bond markets have priced in a reasonably important discount in rates of interest, signally an expectation of a recession within the coming quarters. We might not be stunned by a drop in inventory costs adopted by a powerful restoration by year-end, although different situations are additionally potential.

Extra to the purpose, it’s practically unattainable to time inventory market actions like that. For instance, historic durations when client sentiment concerning the economic system was at its worst have been a few of the finest occasions to purchase shares. Fairness costs are more likely to be unstable this yr as buyers weigh the affect of a looming (or prevented) recession and negotiations in Washington round elevating the debt ceiling, amongst different geopolitical considerations.

Our Portfolios

Our inventory publicity is at present broad primarily based and weighted in direction of massive U.S. firms. Our price bias has helped enhance efficiency regardless of the broad weak point of U.S. inventory markets to date this yr, and usually talking, worth firms are inclined to outperform when rates of interest and inflation are larger. Our worldwide publicity stays balanced between hedged and unhedged investments and advantages from extra engaging valuations than comparable U.S. equities.

As we speak’s larger rates of interest imply that anticipated bond returns going ahead are extra engaging than they have been a yr in the past. Extra importantly, if our expectation of a recession is realized, rates of interest will possible settle again down, offering good returns to bonds ought to shares falter heading right into a recession. Bonds needs to be a greater diversifier this yr, particularly if markets are appropriate in forecasting decrease rates of interest heading into 2024.

In brief, we proceed to count on volatility as buyers put together for a potential recession and modify their estimates for inventory costs accordingly. We’ll use such durations of volatility to rebalance portfolios and choose up shares (or bonds) at discounted costs, to raised revenue from the restoration that has adopted each single market decline for so long as there have been markets.

As all the time, we’re right here for you and are prepared to supply the steerage and planning you count on from us. If in case you have any questions on your investments or your monetary plan, we’d love the chance to debate them with you.

DISCLAIMER:

Previous efficiency is just not a sign of future returns. Data and opinions offered herein replicate the views of the writer as of the publication date of this text. Such views and opinions are topic to vary at any level and with out discover. A number of the info offered herein was obtained from third-party sources believed to be dependable however such info is just not assured to be correct.

The content material is being offered for informational functions solely, and nothing inside is, or is meant to represent, funding, tax, or authorized recommendation or a advice to purchase or promote any forms of securities or investments. The writer has not thought of the funding aims, monetary scenario, or specific wants of any particular person investor. Any forward-looking statements or forecasts are primarily based on assumptions solely, and precise outcomes are anticipated to range from any such statements or forecasts. No reliance needs to be positioned on any such statements or forecasts when making any funding choice. Any assumptions and projections displayed are estimates, hypothetical in nature, and meant to serve solely as a suggestion. No funding choice needs to be made primarily based solely on any info offered herein.

There’s a threat of loss from an funding in securities, together with the chance of complete lack of principal, which an investor will should be ready to bear. Various kinds of investments contain various levels of threat, and there could be no assurance that any particular funding might be worthwhile or appropriate for a selected investor’s monetary scenario or threat tolerance.

Blankinship & Foster is an funding adviser registered with the Securities & Change Fee (SEC). Nevertheless, such registration doesn’t indicate a sure stage of ability or coaching and no inference on the contrary needs to be made. Full details about our providers and costs is contained in our Type ADV Half 2A (Disclosure Brochure), a duplicate of which could be obtained at www.adviserinfo.sec.gov or by calling us at (858) 755-5166, or by visiting our web site.

[ad_2]